Game theory, geopolitics, and the Reinhart–Rogoff mirror

Jorge E. Muro Arbulú

April 2026

Grub first, then ethics.

Bertolt Brecht, The Threepenny Opera (1928)

Abstract

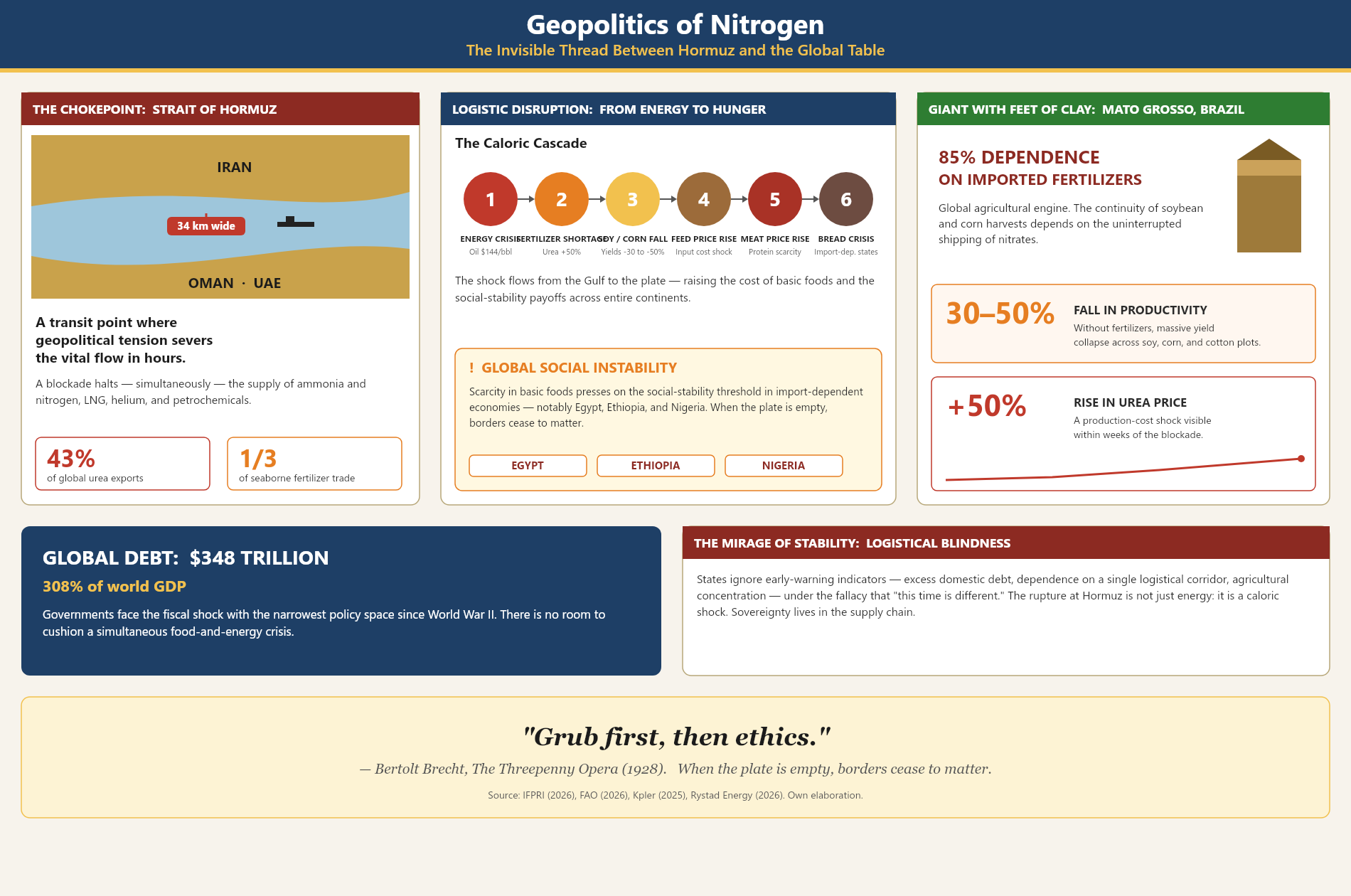

In their seminal analysis of eight centuries of financial history, Reinhart and Rogoff (2009) trace the recurrence of debt crises across 66 countries, refuting the persistent fallacy that “this time is different.” The relevance of that framework is on evident today amid the blockade of the Strait of Hormuz — an event that has revealed a form of logistical blindness to underlying dependencies: from the Qatari helium critical for Taiwan’s microchips, to the Gulf urea that underpins productivity in Mato Grosso. This crisis demonstrates that even the world’s great breadbaskets — which do not produce their own fertilizers and import up to 85% of them — confirm that financial folly translates, inevitably, into a global caloric vulnerability.

The architecture of global food supply reveals a critical asymmetry: the sovereignty of the main exporters is inversely proportional to their autonomy in basic inputs. Mato Grosso, Brazil’s agricultural engine, operates as a giant with feet of clay because it lacks its own fertilizer industry and depends on imports for 85% of its nitrogen, conditioning its soybean and corn production on the stability of maritime flows. At the same time, powers such as the United States and Argentina — despite sitting on vast natural-gas reserves like Vaca Muerta — face an industrial-transformation deficit: the scale of their harvests far exceeds their installed urea-production capacity, forcing them into a global bidding war for processed nitrogen and liquefied gas.

This article links the analytical framework of Reinhart and Rogoff (2009) — built on eight centuries and 66 countries — with the energy, food, and geopolitical crisis unleashed by the blockade of the Strait of Hormuz in March 2026 (IEA, 2026; Kpler, 2026). Drawing on game theory (Nash, 1951; Spence, 1973; Tirole, 2006), it shows that both banking collapse and the emergency hoarding of resources are rational responses to perverse incentive structures. The transmission chain energy → fertilizers → food is analyzed with particular attention to the case of Mato Grosso (Brazil), whose 85% dependence on imported fertilizers turns a maritime blockade into a global food shock. All of this unfolds when the policy space — the governments’ capacity to respond with fiscal stimulus or interest-rate cuts — is the narrowest it has been since the Second World War: global debt reached a record $348 trillion, equivalent to 308% of world GDP (IIF, 2026, cited in Reuters, 2026). The article concludes that the world of 2026 has not escaped the “this time is different” syndrome — it is living it in real time.

Keywords: financial crises, Reinhart–Rogoff, game theory, Strait of Hormuz, geopolitics of nitrogen, Mato Grosso, hoarding, stagflation, sovereign debt, food security.

About the author: Jorge E. Muro Arbulú — PhD in Physics, National University of La Plata, Argentina.

I. Introduction: history as a mirror

“Grub first, then ethics.” — Bertolt Brecht, The Threepenny Opera (1928)

In the early hours of March 18, 2026, Iranian missiles struck the LNG plant at Ras Laffan (Qatar), setting off the largest energy disruption since the 1973 Arab oil embargo. Brent crude surpassed $116 per barrel, touching $144 on the spot market — the price for immediate delivery, as distinct from futures contracts that fix today the price of future deliveries. Traffic through the Strait of Hormuz collapsed by 91%, and the International Energy Agency activated the largest release of strategic reserves in its 50-year history: 400 million barrels, coordinated among more than 30 countries (IEA, 2026; Kpler, 2026).

But the energy shock was only the first link. The blockade also cut off the flow of fertilizers. Roughly one-third of the world’s seaborne urea and ammonia trade transits the Strait of Hormuz (Dart, 2026, cited in Euronews, 2026). The disruption directly threatens the harvests of Mato Grosso — Brazil’s agricultural heartland, which imports 85% of its fertilizers. Within weeks, urea prices rose by roughly 50%.

If soybean and corn production in Brazil contracts, the effect propagates in a chain. Feed becomes more expensive, then meat, and finally bread. In countries such as Egypt, Ethiopia, or Nigeria, that chain presses on social stability up to a threshold at which, with an empty plate, borders cease to matter.

All of this is happening alongside an unprecedented fiscal fragility: global debt reached $348 trillion — 308% of world GDP — with nearly $29 trillion added in 2025 alone, the fastest accumulation pace since the pandemic (IIF, 2026, cited in Reuters, 2026). For the first time in modern history, the United States pays more in interest on its debt ($1 trillion) than in its defense budget ($885 billion).

This scenario would not have surprised Carmen Reinhart or Kenneth Rogoff. In This Time Is Different: Eight Centuries of Financial Folly, they showed that crises are not accidents — they are the predictable result of institutional forgetting and of incentive structures that make rational what is socially destructive (Reinhart & Rogoff, 2009). This article uses that framework, enriched with game theory, to analyze the 2026 crisis not as an exceptional event, but as the latest iteration of an eight-century cycle.

II. The central thesis: the “this time is different” syndrome

Reinhart and Rogoff (2009) identify a recurring pattern: during credit booms, economic agents convince themselves that the rules that produced earlier crises no longer apply. This illusion takes various forms: “our institutions are more modern,” “monetary policy is now more rigorous,” “markets are more liquid.” The result is invariably the same.

The authors identify three dimensions of the syndrome:

- The cycle of institutional forgetting. The lessons of previous crises erode during booms, eliminating early-warning mechanisms precisely when they are most needed (Reinhart & Rogoff, 2009).

- The universality of the phenomenon. Banking crises are not the preserve of emerging economies; they have struck advanced economies — including the G7 — with equal intensity (Reinhart & Rogoff, 2009).

- The massive and invisible social cost. The deepest effects — falling employment, deterioration of public services — manifest with lags of months or years relative to the initial shock (Reinhart & Rogoff, 2009).

In 2026, the modern equivalent of the syndrome is the conviction — held through a decade of ultra-expansionary monetary policy — that debt at near-zero rates was sustainable indefinitely. Global public debt surpassed 93% of GDP in 2024, compared with 20% for the G7 in the 1970s (IMF, 2025), and no corrective mechanism was triggered.

III. Typology and dynamics of crises: 800 years of evidence

3.1 External debt, banking crises, and the 86% pattern

Reinhart and Rogoff (2009) show that public debt rises by an average of 86% in the three years following a banking crisis. This is the book’s most-cited quantitative finding — and also the one most consistently ignored by policymakers at the moment of the bailout. The fiscal repercussions are systematically more costly than the bank rescues themselves: governments save the banks, but remain trapped in the debt that the rescue generates.

| Country / bloc | Public debt (% GDP), 1970s | Public debt (% GDP), 2025 | Change |

|---|---|---|---|

| G7 (average) | ~20% | >100% | +80 pp |

| United States | 35% | 122% | +87 pp |

| Japan | 15% | 260% | +245 pp |

| Germany | 18% | 65% | +47 pp |

| Italy | 35% | 137% | +102 pp |

| Crisis / episode | Increase in public debt (3 years post-crisis) | Observation |

|---|---|---|

| 800-year historical average (R&R, 2009) | 86% | Central finding |

| Nordic banking crisis (1991–1993) | 75% | Sweden adopted deep structural reforms |

| Asian crisis (1997–1998) | ~100% | Regional contagion through the exchange rate |

| Global financial crisis (2007–2009) | ~90% | U.S.: housing and current-account imbalances above prior averages |

| Hormuz crisis 2026* | To be determined | Global debt: $348 T; U.S. deficit ~7% of GDP; no policy space left |

3.2 Debt intolerance

Analyzing the sustainability of public finances, Smith (1776/2007) wrote that “when national debts have once been accumulated to a certain degree, there is scarce, I believe, a single instance of their having been fairly and completely paid” (p. 819). Reinhart and Rogoff (2009) coin the term debt intolerance: countries that default even at debt levels that would be apparently manageable for other economies, because of their accumulated institutional weakness. This phenomenon means that the same debt level can be sustainable for Germany and unsustainable for Argentina — not because the numbers differ, but because institutional credibility, built over decades, does.

3.3 Inflation as covert default

Historically, governments have resorted to inflation as a covert default mechanism on domestic debt (Reinhart & Rogoff, 2009). This “financial repression” was the dominant debt-reduction mechanism in the decades after World War II. In 2026, with interest rates elevated to contain post-pandemic inflation, this tool is not available without aggravating other imbalances: cutting rates to liquidate debt is equivalent to fanning the inflation already driven by oil and fertilizers.

IV. The game-theoretic dimension

What Reinhart and Rogoff (2009) call “folly” — the repetition of errors over eight centuries — can be understood as the outcome of non-cooperative equilibria among rational agents operating under perverse incentive structures (Nash, 1951). Folly is not irrational: it is the logical consequence of playing with the wrong incentives.

4.1 The banking prisoner’s dilemma

During credit booms, banks face a classic prisoner’s dilemma (Nash, 1951). If one bank adopts a prudent stance while the others keep expanding, it loses market share and shareholders. The dominant strategy is to continue expanding credit. The resulting Nash equilibrium is one in which all banks are over-exposed, generating the systemic risk that precipitates the collapse. Macro-prudential regulation cannot rely on self-regulation of agents: in the absence of coercive coordination, the individually dominant strategy will always produce the systemically dangerous equilibrium.

| Bank B: Prudent | Bank B: Expands credit | |

|---|---|---|

| Bank A: Prudent | A gains little, B gains little (social optimum) | A loses market share, B gains a lot (A punished) |

| Bank A: Expands credit | A gains a lot, B loses market share (B punished) | NASH EQUILIBRIUM — Both over-exposed → systemic collapse |

4.2 Time inconsistency and dynamic games

The second mechanism is time inconsistency (Tirole, 2006). Governments promise fiscal and monetary discipline when they access credit, but once they have accumulated debt, they have an incentive to renege via inflation or restructuring — exactly the mechanism documented by Reinhart and Rogoff (2009) over eight centuries. Markets anticipate this dynamic and price in a risk premium from the outset. Institutional credibility is the scarcest asset: the one that takes longest to build and is fastest to destroy.

4.3 Asymmetric information and signaling

The concept of debt intolerance can be analyzed as a signaling problem in markets with asymmetric information (Spence, 1973). A country with a history of defaults tries to signal that “this time is different,” that its institutions are more solid. However, Reinhart and Rogoff’s (2009) 800-year database acts as a stronger and more credible signal than any policy declaration: markets assign greater weight to track record than to stated intent.

4.4 The hoarding dilemma: a new Nash equilibrium

The 2026 crisis generates a second prisoner’s-dilemma structure that Reinhart and Rogoff (2009) did not analyze directly, but that their framework anticipates: the hoarding of critical resources under scarcity. China banned exports of gasoline, diesel, and jet fuel on March 11, 2026, by order of its National Development and Reform Commission (NDRC); India — which had already restricted rice exports in 2022 under similar shocks — now faces in 2026 a domestic liquefied petroleum gas (LPG) shortage that pushes in the same direction (CNN, 2026; Martín-Rayo, 2026). The resulting Nash equilibrium is a global scarcity spiral that reduces the welfare of everyone, including those who hoard.

| Country B: Does not restrict exports | Country B: Restricts exports | |

|---|---|---|

| Country A: Does not restrict | A: moderate risk; B: moderate risk (cooperation — global optimum) | A: severely harmed; B: protected in the short term |

| Country A: Restricts exports | A: protected in the short term; B: severely harmed | NASH EQUILIBRIUM — Both restrict → global scarcity spiral |

V. The Hormuz crisis: the nitrogen chain and hunger

5.1 From Hormuz to Mato Grosso: the invisible chain

The 2026 Hormuz crisis illustrates the contagion mechanism documented by Reinhart and Rogoff (2009), but through physical supply chains rather than the banking system. The blockade of the strait did not just interrupt the flow of oil: it simultaneously stopped LNG, fertilizers, helium, and petrochemicals (IEA, 2026; Kpler, 2026).

The critical link is nitrogen. Approximately one-third of the world’s seaborne fertilizer trade transits the Strait of Hormuz, including 43% of urea exports and 44% of sulfur (Dart, 2026, cited in Euronews, 2026). Mato Grosso — Brazil’s largest agricultural state and one of the world’s leading producers of soybeans and corn — imports 85% of its fertilizers. Without them, agricultural output falls by 30% to 50% depending on crop and soil. Of the potassium feeding those fields, 95% — and 80% of the nitrates — depend on invisible geopolitical threads that pass through a 34-km strait.

The transmission chain is exactly the one Brecht described before modern geopolitics existed: without fertilizers, no soybeans or corn in Mato Grosso; without soybeans or corn, feed prices rise; without affordable feed, meat becomes a luxury; without accessible protein, bread in Egypt, Ethiopia, or Nigeria becomes unreachable. When the plate is empty, borders cease to matter — and migratory pressure becomes the political crisis of the next chapter.

| # | Link | Event / shock | Consequence / source |

|---|---|---|---|

| 1 | Energy | Strait of Hormuz blockade (~6 weeks) | Oil at $144/barrel; traffic −70% (IEA, 2026; Kpler, 2026) |

| 2 | LNG / helium | Ras Laffan out of service | 25% of global LNG interrupted; helium +30% (Chávez Calva, 2026) |

| 3 | Fertilizers | Urea and ammonia with no sea route | Urea price +50%; one-third of seaborne fertilizer trade via Hormuz (Dart, 2026, in Euronews, 2026) |

| 4 | Mato Grosso / Brazil | 85% of imported fertilizers suspended | No inputs for soy and corn; potassium and nitrates at critical supply levels |

| 5 | Global food | Falling agricultural yields | Feed → meat → bread; instability in Egypt, Ethiopia, Nigeria |

| 6 | Hoarding | China bans gasoline/diesel exports; India tariffs | Inefficient Nash equilibrium: local protection reduces global welfare |

| 7 | Pharmaceutical | Petrochemical chain fractured | Pressure on active ingredients; helium for MEG/MCG (IEA, 2026) |

| 8 | Fiscal / debt | Bailouts + revenue loss | Public debt +86% in 3 years — the historical pattern (Reinhart & Rogoff, 2009) |

| 9 | Migration | Hunger in the Mediterranean and Africa | When the plate is empty, borders cease to matter |

| 10 | Geopolitical | Realignment of alliances | U.S. eases sanctions on Russia; Vaca Muerta surges (IEA, 2026) |

5.2 The mirage of the ceasefire

The 14-day truce announced between the United States and Iran — mediated by Pakistan, with partial reopening of the Strait of Hormuz where 800 ships are waiting — illustrates the mechanism Reinhart and Rogoff (2009) describe as the confusion of a pause with a resolution. A temporary interruption of the armed conflict does not repair fractured supply chains, does not lower the urea price that has already risen 50% (Dart, 2026, cited in Euronews, 2026), does not replenish hospital helium inventories (Chávez Calva, 2026), and does not restore the confidence of maritime insurers — which have classified the entire Persian Gulf as a zone of “maximum war risk.” In addition, the U.S. president has warned that, if the agreement is not “good,” the conflict will be resumed. This ambiguity is precisely the kind of signal that Spence (1973) identifies as incapable of generating credible commitments.

VI. The erosion of economic policy space

6.1 Nixon 1973 vs. the Trump administration 2026

The concept of policy space — the ability of governments and central banks to respond to a crisis through fiscal stimulus, interest-rate cuts, or liquidity injections — is today the narrowest it has been since World War II. The difference between 1973 and 2026 does not lie in the magnitude of the initial shock but in the tools available to cushion it.

In 1973, when the Arab embargo set off the first oil crisis, the public debt of the G7 countries1 was below 20% of GDP. Governments could resort to fiscal expansion because they had room. In 1979, Volcker’s Federal Reserve could raise interest rates drastically because it started from levels that — though elevated — still had headroom. In 2026, none of those options is available without worsening other imbalances: public debt exceeds 100% of GDP across the entire G7, the U.S. fiscal deficit is around 7% of GDP, and U.S. debt-interest payments — $1 trillion — for the first time exceed the $885 billion defense budget (IIF, 2026, cited in Reuters, 2026).

This creates what, from the perspective of Nash (1951), is a player constraint: the United States can no longer behave as an actor with unlimited resources at the negotiating table. Its constant refinancing need raises the opportunity cost of sustaining a protracted conflict. Increased military spending to confront the Iran crisis widens the deficit, which raises Treasury yields, which in turn makes debt service more expensive — closing the vicious circle that Reinhart and Rogoff (2009) documented across dozens of historical episodes.

1 Germany, Canada, the United States, France, Italy, Japan, and the United Kingdom.

| Indicator of policy space | Nixon / Carter 1973–1979 | Hormuz crisis 2026 | Source |

|---|---|---|---|

| G7 public debt (% GDP) | ~20% | >100% ↑ | IMF (2025); IIF (2026, in Reuters, 2026) |

| Total global debt | ~$100 T | $348 T ↑ | IIF (2026, in Reuters, 2026) |

| Global debt (% world GDP) | ~150% | 308% ↑ | IIF (2026) |

| U.S. debt interest | Below defense spending | > Defense spending ↑ | IIF (2026) |

| Fed interest rates | Room to raise | Elevated — no room ⇄ | Reinhart & Rogoff (2009); IIF (2026) |

| IEA oil reserves | Abundant | 400 M barrels (~4 days) ↓ | IEA (2026) |

| U.S. fiscal deficit (% GDP) | ~2% | ~7% ↑ | IMF (2025) |

VII. Wartime stagflation and the central-bank paradox

The resulting scenario — a severe energy shock with record global debt and fractured physical supply chains — creates a trap with no apparent exit for central banks, which economists call stagflation: simultaneous inflation and stagnation. The peculiarity of 2026 is that it is a wartime stagflation, in which inflation arises not from excess demand but from a physically broken supply (Tirole, 2006).

Under this scenario, conventional instruments lose their effectiveness:

- If the central bank raises rates to fight imported inflation (energy, fertilizers, food), it deepens the recession and raises the cost of sovereign debt service, pushing several countries toward the insolvency threshold documented by Reinhart and Rogoff (2009).

- If it cuts rates to stimulate growth, it fuels inflation expectations and erodes the credibility painstakingly built through the 2022–2024 hikes — reproducing the time inconsistency described by Tirole (2006).

- If it does nothing, inflation entrenches, real wages fall, and social tension and political pressure mount on independent institutions.

The European Central Bank has warned that Germany and Italy could enter technical recession before the end of 2026. In this context, the divergence between small, disciplined economies — Sweden, Taiwan, Vietnam, with deficits below 2% of GDP — and the large, indebted G7 economies illustrates the central principle of Reinhart and Rogoff (2009): “debt intolerance” is a continuum, and countries that have kept arithmetic rigor have more room to absorb the shock.

VIII. Strategic conclusions

8.1 The fallacy of “this time is different” in state planning

The main conclusion of this analysis, supported by eight centuries of evidence (Reinhart & Rogoff, 2009), is that institutional stability is often a mirage fueled by the credit boom. States tend to ignore early-warning indicators — excess domestic debt, dependence on a single logistical corridor, the concentration of agricultural output in a single geographic point — in the belief that their current policies are immune to the past. A country’s “graduation” — its capacity to overcome crisis cycles — is not a permanent state but a fragile process that can be reversed by a mismanaged crisis.

8.2 Sovereignty lives in the supply chain

Analysis of the 2026 crisis shows that sovereignty does not reside solely in borders but in the continuity of supply chains (IEA, 2026). The 85% dependence on imported fertilizers in agricultural powers such as Brazil reveals a structural vulnerability that no amount of military spending can compensate for in the short term. The rupture at the Strait of Hormuz is not just an energy problem: it is a food shock that alters the payoffs of social stability across entire continents, from the Mediterranean to sub-Saharan Africa. The geopolitics of nitrogen — systematically ignored in conventional risk analysis — can be as decisive for social peace as the geopolitics of oil.

8.3 Modeling decisions under radical uncertainty

From the perspective of game theory (Nash, 1951), today’s crises present themselves as games of asymmetric information and failed cooperation. The hoarding dilemma — where each actor’s dominant strategy generates a globally inefficient equilibrium — is the 2026 version of the banking prisoner’s dilemma that triggered the financial crises of earlier centuries (Reinhart & Rogoff, 2009). The difference is that the damage no longer accumulates on bank balance sheets: it accumulates in empty silos and in the empty shelves of supermarkets.

The real world is not explained with headlines; it is explained with the stability of the chains of oil, nitrogen, and grain. When one link breaks, the whole chain tenses. And the history of eight centuries shows that there will always be someone who says that, this time, the link will not break.

References

- International Energy Agency (IEA). (2026). Oil Market Report, March 2026. IEA. https://www.iea.org/reports/oil-market-report-march-2026

- Brecht, B. (1928). The Threepenny Opera [Stage play]. Premiere at the Theater am Schiffbauerdamm, Berlin.

- Chávez Calva, J. L. (2026, March 13). Shock de helio 2026: el conflicto con Irán detiene la producción de Qatar y duplica los precios spot. Substack. https://joseluischavezcalva.substack.com/p/shock-de-helio-2026-el-conflicto

- Dart, S. (2026, March). Note on LNG disruptions in the Persian Gulf [Research note]. Goldman Sachs Research. Cited in Euronews (2026, March 17). https://es.euronews.com/business/2026/03/17/guerra-en-iran-se-revelan-las-empresas-ganadoras-y-perdedoras-en-europa

- Food and Agriculture Organization of the United Nations (FAO). (2026, March 26). FAO Chief Economist warns of severe global food security risks from disruption to Strait of Hormuz trade corridor [Statement by Máximo Torero, Chief Economist]. FAO Newsroom. https://www.fao.org/newsroom/detail/fao-chief-economist-warns-of-severe-global-food-security-risks-from-disruption-to-strait-of-hormuz-trade-corridor/en

- International Monetary Fund (IMF). (2025, September 17). Global debt remains above 235% of world GDP [Blog post]. IMF. https://www.imf.org/en/blogs/articles/2025/09/17/global-debt-remains-above-235-of-world-gdp

- Institute of International Finance (IIF). (2026, February 25). Global Debt Monitor: Q4 2025. IIF. Cited in Reuters (2026, February 25). https://www.investing.com/news/economy-news/government-spending-lifts-global-debt-to-a-record-348-trillion-in-2025-says-iif-4524935

- Kpler. (2026). Strait of Hormuz maritime-traffic data (March 2026). Kpler Analytics. https://www.kpler.com

- Martín-Rayo, F. (2026, March 24). Disruptions at the Strait of Hormuz are triggering a slow-simmering food crisis. The Wall Street Journal. https://www.freshfruitportal.com/news/2026/04/06/hormuz-food-crisis/

- Nash, J. (1951). Non-cooperative games. Annals of Mathematics, 54(2), 286–295. https://doi.org/10.2307/1969529

- QatarEnergy. (2026, March 18–19). Official statements on the attacks on the Ras Laffan and Mesaieed facilities. https://www.qatarenergy.qa

- Reinhart, C. M., & Rogoff, K. S. (2009). This Time Is Different: Eight Centuries of Financial Folly. Princeton University Press.

- Smith, A. (1776). An Inquiry into the Nature and Causes of the Wealth of Nations.

- Spence, M. (1973). Job market signaling. The Quarterly Journal of Economics, 87(3), 355–374. https://doi.org/10.2307/1882010

- Tirole, J. (2006). The Theory of Corporate Finance. Princeton University Press.